An ecosystem that is becoming more structured, business models that are still being sought

Summary

Hybridization of funding sources

The most striking fact is the multiplicity of funding sources:

- 72% of the structures use public subsidies to finance their activities.

- 47% use sales and services

- "Proof of the importance of the associative model in the ecosystem, memberships and contributions also represent a source of revenue for 36% of the structures.

The authors of the study point to " the low share of financing through loans or investments (8% in all), which is probably explained by the fact that the majority of private structures in the digital inclusion sector have associative status, but also by the structural and historical insufficiency of financing for social innovation in France, which is still perceived as too risky and not profitable enough in the short term.

The mix of funding combining public support from various sources, own resources via service provision, and citizen contributions" is fairly typical of the social and solidarity economy ecosystem.

"It is clear," the authors add, " that this hybridization in economic models is imperative in order to move towards a balanced budget in the long term.

In this hybridization of funding sources, "majority mixes" emerge, notably between public subsidies and the sale of services, which share the top spot.

An analysis of the survey responses reveals the importance of calls for projects or calls for expressions of interest in the "funding mix" of actors. Thus, more than 1/3 of the actors use them and for 1/3 of them, they represent their first or second source of funding. "Such a proportion perfectly illustrates the fragmentation of funding and the prevalence of a non-permanent, piecemeal support logic. The multiplication of interlocutors and funding mechanisms, project by project, is a source of complexity and exhaustion for the players in the ecosystem. The actors are well aware of the limits of this way of working, which does not allow them to plan for the long term.

Local authorities, first financial partners

While the stimulus plan has strengthened existing funding at the national level (notably with the deployment of the Digital Pass and the structuring of territorial hubs), local authorities are among the leading funding partners for digital inclusion activities and structures.

Thus, among the actors supported by the public authorities, 53% say they are financially supported by departments, 41% by municipalities, 33% by EPCIs and 32% by regions.

The use of European Union funds is still too modest for the moment (18%).

According to the authors of the study, " the strong presence of public funding should gradually be rebalanced by private demand, especially via the growing need for digital training of corporate employees."

Driven by the Personal Training Account (PTA) and by certifications dedicated to basic digital skills, digital mediation activities could be deployed for employees, with several methods of remuneration for mediation actors: by the employing company, by the employee's PTA, by the employing state or even by the civil servant's PTA

Financing remains a concern for industry players.

57% of the ecosystem players point to the lack of funding as a hindrance to their development.

"This issue of financing actually covers several subjects. First, the insufficiency of public support, the complexity and dispersion of public funding (multiple calls for projects, calls for expressions of interest and access to grants). As well as the difficulty in finding private funding or convincing investors to support their development.

Communities, full-fledged players in the ecosystem

For the past twenty years, many communities have implemented digital inclusion policies adapted to their local challenges. "Digital inclusion is not a competence reserved for one level of government, and each level is supposed to act in this field and bring its added value according to local dynamics.

- Among the communities that responded to the questionnaire, municipalities and inter-municipalities represent more than 74% of the communities involved.

- More and more departments are also getting involved in these digital inclusion issues. They represent 19% of the responding communities.

The average budgets dedicated to digital inclusion vary greatly from one level to another and correspond to their ability to commit funds. 75,000 per year on average, the departments are able to allocate larger budgets, approaching an average of

New actors

The growing social needs and the mobilization of public funds have attracted, for a few years now, new actors, who were not previously involved in digital mediation, such as the Red Cross, neighborhood associations, independent digital mediators

The survey found that 66% of organizations that do not have digital inclusion as their primary activity started these activities 5 years ago or less.

An ecosystem that is becoming more structured

"The ecosystem now needs to be better structured to ensure better coordination of its various players and to enable its necessary scaling up. This structuring is being carried out around, in particular, the Mednum and the various territorial Hubs for an inclusive digital environment.

The Mednum was born, in 2017, at the initiative of about forty actors of digital inclusion and the State. It gathered 118 members throughout the territory in September 2022.

Noting the lack of an intermediary tier between national actors and local digital inclusion structures, the Banque des Territoires and the National Agency for Territorial Cohesion launched a first call for expressions of interest in 2018 to create the first Territorial Hubs for Digital Inclusion - structures with the vocation of being true local network heads for digital inclusion.

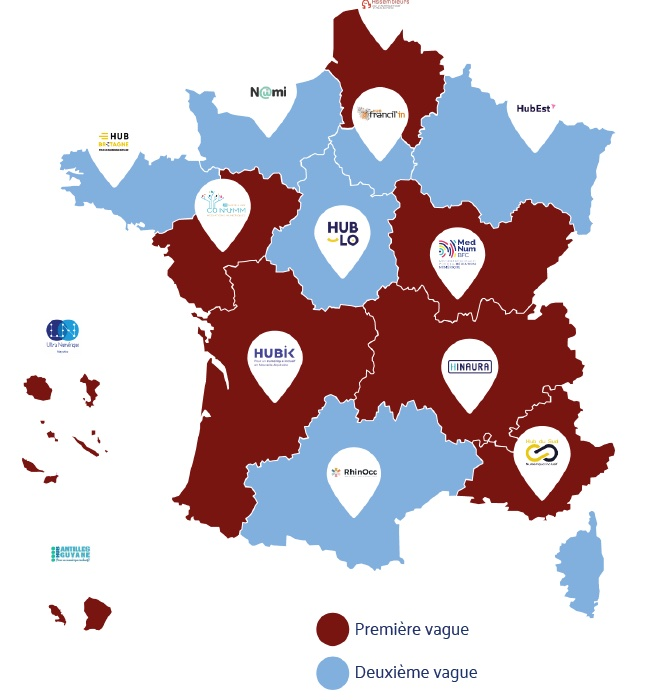

11 Hubs are labeled in the first wave:

- The Assemblers in Hauts-de-France,

- Francil'IN in Île-de-France,

- Conumm in Pays-de-la-Loire,

- The Hub-Lo in Centre-Val-de-Loire,

- Mednum BFC in Bourgogne-Franche-Comté,

- Hubik in New Aquitaine,

- Hinaura in Auvergne-Rhône-Alpes,

- Rhinocc in Occitania,

- The Southern Hub in Provence-Alpes-Côte-d'Azur,

- UltraDigital in La Réunion-Mayotte,

- And the Antilles-Guyana Hub.

A second wave of the AMI, conducted in 2021, has enabled new Hubs to emerge and cover the entire territory:

- The Hub of Brittany,

- The Normandy Hub,

- The Hub of the Great East,

- And the Hub of Corsica.

The main mission of the Hubs is to coordinate and animate networks of actors, as well as to support local authorities in developing digital inclusion projects (mapping, project engineering, fundraising...).

"If the Hubs system works well in territories that are already organized and rather mature in their digital inclusion approaches, some of them still encounter difficulties in setting up and being recognized by local actors, making the territorial visibility of the sector still partial.

However, the hubs rely on a fragile economic model: "Indeed, beyond the 18 months during which they benefit from a state subsidy, they must find their own sources of funding from public or private actors. This financial autonomy seems difficult to achieve for those located in territories with little structure in terms of digital inclusion.

In this perspective of networking and cooperation between actors, the Digital Society mission of the ANCT has recently launched The BaseThe Base is a platform that brings together all the resources for digital inclusion and mediation. "Its objective is to allow all the actors of the sector to easily identify tools and resources that are useful to them on a daily basis, by facilitating new collaborations between them in a growing logic of emergence of digital commons.

Référence :